June 2026 Portfolio Review

Here's What I've Been Buying and Selling

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

You’re not losing your mind. If it feels like things are crazy, that’s because they really are. As crypto seemingly fades into irrelevancy, its knee-jerk moves have insidiously become commonplace to metals, megacaps, and even traditionally boring sectors such as consumer staples and insurance.

Part of the reason, to borrow a phrase from the President, is because “everything is computer”. Gross hedge fund exposure and median short interest are near record highs as investors pile into the AI Trade and discard everything else.

The chart above from Goldman Sachs’s Prime Brokerage Desk depict stunning gross and net concentration in Semis, and the continued pile-on into the AI trade has caused cross-sector correlations to go haywire. To see that exemplified, look no further than the insurance sector. For the first time ever, the insurance sector (KIE) is negatively correlated with the S&P on a 40 day rolling basis.

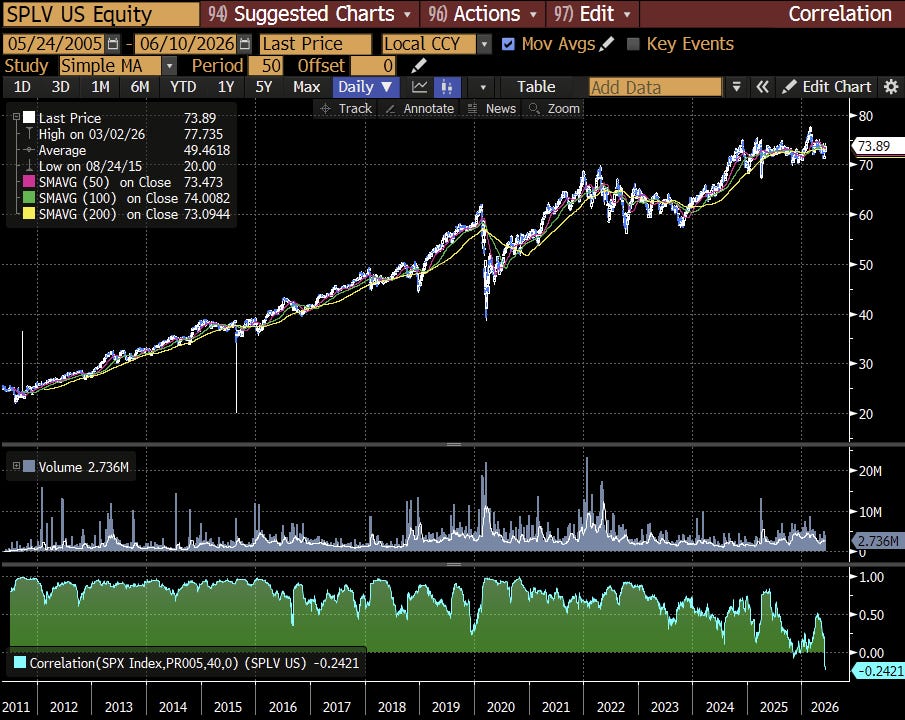

The S&P Low Volatility Index has similarly become negatively correlated with the S&P.

It’s not like AI has magically become the ultimate enemy of insurers, banks, and consumer staples businesses in the span of two months, rather, these wild moves and cross-sector correlations are the result of positioning: people are pressing the pedal to the metal on the AI trade by paring down everything else, and when they degross, the unwind gets violent quickly. From Wednesday June 3rd through Wednesday June 10th, the Semiconductor Index was down 10% while Banks rallied up 5%. If you’re looking for an explanation, look no further than the fact Institutional positioning in Financials started the month at the 0th percentile (in relative terms since 2010), while Information Technology started the month off at the 99th percentile (source: Morgan Stanley Prime Brokerage Desk).

Given the recent volatility, I think it’s fair to say many investors are aggressively exposed with complicated positions. The question is, what should we do?

I think the answer is clear: keep things simple until everyone calms down.

Since April I’ve been trying to do as little as possible and avoid working myself up into a frenzy. If you interpreted every Iran or Tech headline at face value, you’d wind up in the insane asylum.

I think the same goes for deciding whether to buy the dip. A lot of recent market action seems to be driven by recency bias, people looking at where a stock was merely two or three days ago, and using the differential to decide whether to go “all in” or “all cash”.

I think the memory names exemplify this well. In the depths of April, Turboquant nearly made its way onto the terrorist watchlist - it was panic like never before. If you asked stunned memory bulls (including myself) if they’d be willing to take off some Micron at $550 or $600 if it ever returned, the answer would’ve been an clear yes. “Oh if you let me get out of this hole, I’ll never take risks like that again”.

Now, Micron has more than tripled to $900, yet people aren’t merely maintaining their positions, they’re aggressively piling in because it was $1,080 a few days ago. If you’re scooping up shares because you believe Micron will hit a $30 a quarter run rate by Q3 and memory is no longer cyclical, I tip my hat to you, but otherwise, I think it’s okay to say “You know what, it’s up 200% YTD, a little volatility is to be expected and I don’t need to buy this dip”.

This year the volatility has been immense. The crown has rotated from Gold and Silver connoisseurs to Small Cap Oil Experts to Korean Memory Superfans, over and over and over again. Rather than chase, I think the best thing to do is just purchase reasonably priced equities with decent growth prospects and capital return potential, and let time put in some work.

My Portfolio is relatively untouched since the last update in April, but I have been adding to a few existing positions and collaring a few I view most at risk. Here’s what I’ve been up to.