Kazakhstan, Japan, and Trimming a Winner

A 9% Yield for a "Growth" Name, Using Share Repurchase Reports to Time "Dip Buys", and Trimming a Winner

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

Kazakhstan

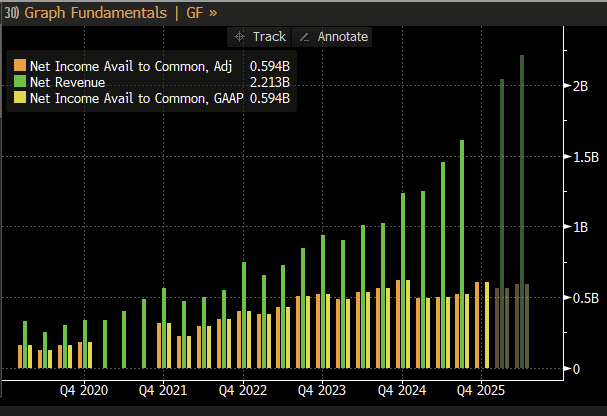

Kaspi KSPI 0.00%↑ reported earnings of $2.76, missing the consensus of $3.34 due to higher taxes and bank reserve requirements impacting its Fintech division, but there is more to the story here.

For several quarters Kaspi has been plagued by an absence of capital returns as it poured billions into its acquisition of Hepsiburada(the second largest E-commerce firm in Turkey). Now, Kaspi is finally turning its attention back onto the shareholders.

Letter from Mikhail Lomtadze:

Two topics have dominated my conversations with investors over the last year: our progress in Türkiye and our approach to dividends. I want to address these and the other questions we hear most often, so that you better understand the context behind the decisions we’re taking.

Both Türkiye and dividends connect to a single ambition: to build Kaspi.kz into a 100 million user company. We believe that every strategic decision we make – the launch of new products and services, investments in Türkiye, and dividend policy – is anchored to this goal.

Earlier today, Kaspi announced an 850 KZT dividend per ADS, which translates into roughly $1.71 at the current exchange rate. The company also stated it believes this dividend is now the baseline going forward.

Based on the business's current performance and cash generation, we believe this is sustainable for the remainder of 2026.

Absent any exchange rate fluctuations, $6.84 in annual dividends represents a roughly 9% yield, immediately vaulting Kaspi from a flailing “value trap” into a cash cow.

Even after lowering my 2026 EPS estimate to $11.75 USD (sharply below the $13.08 consensus), due to more stringent regulations on the banking sector and a higher effective tax rate, Kaspi at 6.5x earnings and a 9% dividend yield still represents a compelling setup.

Kaspi is a “superapp” in Kazakhstan, their proprietary payments, e-commerce marketplace, travel, lending, and grocery divisions dominate the country. Practically every Kazakh adult uses Kaspi. While the government has taken action to “open up” Kaspi’s QR payments division (to allow clients with bank accounts at other institutions to also receive payments), Kaspi’s position in e-commerce is unchallengeable, and remains highly linked to a growing Kazakh economy.

With a massive 9% dividend yield now in place, I believe the bottom for Kaspi is finally in. Kaspi is a growth name trading at a deep-value multiple, and I think the recent share buyback program paired with the long-awaited resumption of the dividend is finally enough to change the narrative. I have increased my position to 2% of my portfolio, and have orders to buy more in the $70-$75 range should it trade down in the coming days - Kaspi is a high conviction name for me. Based on the current multiple and implied 9% yield, I think a more reasonable valuation for Kaspi would be $90 a share, implying a 7.5% dividend yield and 7.5x 2026 earnings.

Japan

A lot of times I get asked if “it’s still a good time to add to Japanese positions”. It’s a good question, the Topix is up 50% in the last year and many Japanese Banks and value setups that previously traded at just 5-6x earnings now trade at 10-12x/ It’s hard to determine if the setups are still compelling at first glance.

An excellent guiding point, however, is if the company finds its own shares attractive. Unlike US-listed equities where share repurchases are reported quarterly, Japanese-listed equities announce share repurchase authorizations and buyback activity on a monthly basis, with detailed reports denoting the exact price and volume executed on an individual day reported at the end of the month.

While these disclosures mildly complicate buybacks since they tend to “tip the hand” of the company to investors (sometimes leading to buybacks being massively front run), they provide an excellent way to determine if a company still has an “appetite” for its shares after a run up in price.

One of the names we discussed last summer has been on an impressive 50% run, but February’s repurchase report indicates their appetite is just getting started and the setup is still highly compelling at just 0.61x Tangible Book Value.