Too Many Cooks Spoil The Pot

A Special Situation Setup

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

Too many cooks spoil the pot.

The actual adage is too many cooks spoil the broth, but either way, it’s one of my favorite sayings. This trade is perhaps a financial representation of the adage.

“And we’re off, SpaceX opens at $180 a share up 30%, a valuation of $2.2 Trillion” a Bloomberg anchor quips as he bangs his pen on the circular table. “Really incredible isn’t it, one of the largest IPOs of the year”.

Social media goes wild. One Twitter user adamantly declares he is switching to the S&P 500 Sharia ETF (which excludes Defense Contractors) to avoid his nest egg being invested in SpaceX. Another Twitter user angrily laments “Look at that opening pop, the investment bankers left Hundreds of Billions on the Table! They have no idea what they are doing!” (he has no idea that the opening jump is, in fact, intentional). A third user quickly changes his handle to “SpaceXExpert”, plows his Robinhood account all-in at the opening print, and promptly starts a paid community to exclusively cover all things relating to SpaceX. To top it all off, Defiance promptly files for a 2x SpaceX ETF at 4:05 PM.

You scoff and shake your head, but your smirk quickly turns emotionless as you realize S&P removed the four-quarter profitability test to ensure 1.25% of your SPY money is blindly plowed into SpaceX six months from now.

“Aw f**k”, you mutter.

Now, I’m not saying this is exactly how the SpaceX IPO will go next Friday, June 12th. But if you use your imagination you can see it happening, can’t you?

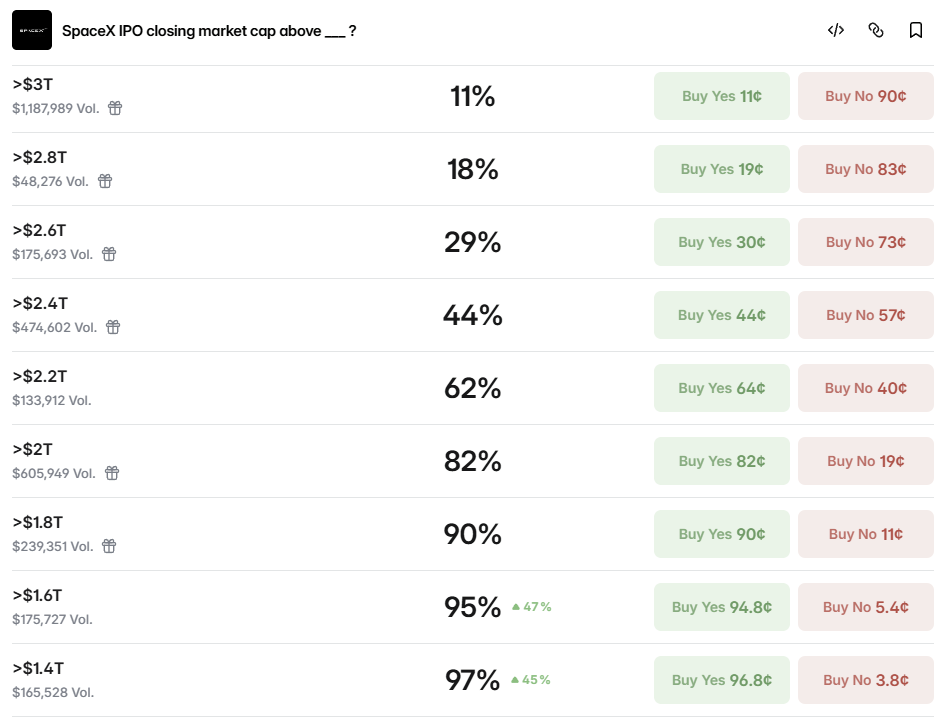

Prediction Markets seem to believe it’s likely SpaceX closes above the $2 Trillion Valuation mark at the end of the session, and Hyperliquid’s Pre-IPO Perpetuals have the stock at roughly $188 a share, approximately 40% higher than the 135 a share SpaceX is currently discussing with banks.

Hyperliquid and Polymarket are by no means accurate indicators, but both, combined with the general excitement for tech IPOs we have seen, lead me to believe the bulls are getting ready to rumble and eventually cram SpaceX into every major index ETF.

It all seems so silly, doesn’t it?

Unless lightning strikes and the IPO allocators at Robinhood pity you enough to toss you a share, or perhaps you’re an Institutional client with a salesperson who finds you to be good company, chances are you aren’t getting an allocation and will have to watch the spectacle from the backrow with a “mental” position.

But imagine if you could make money off this by picking up some SpaceX exposure at a discount to the underwriting price?

Alarm bells should be immediately ringing in your heads. How?

The answer is a vehicle the average speculator hasn’t even considered.

Mutual funds.

There are two mutual funds, BARAX (Baron Asset Fund Retail Class), and BGAFX (Baron Global Opportunity Fund) that have significant SpaceX exposure and are still open to investors. Roughly 24.9% of BARAX (as of April 30, 2026) and 16.3% of BGAFX (as of April 30, 2026) are invested in SpaceX, with the SpaceX shares held at a likely 1.25 Trillion valuation.

“The Fund’s largest holding, Space Exploration Technologies Corp. (SpaceX), appreciated 24.5% in the quarter. SpaceX announced the merger with X.AI Holdings Corp. (xAI) in February. As a result of the deal, the implied value of SpaceX increased to $1 trillion while xAI remained constant to its last financing round at a $250 billion valuation. The combined company is now valued at $1.25 trillion.” - Baron Funds Q1 2026 Letter

What this means in simple terms is that if SpaceX opens at a $1.75 Trillion or a $2 Trillion valuation, both funds will see a significant uplift in Net Asset Value as the position is marked at the closing price on IPO day.

Surprisingly, unlike Neuberger Berman’s NBSRX fund (9% of assets in SpaceX) that has closed itself to new investors (to avoid special situations traders swooping in to add SpaceX exposure for themselves before a big payday), Baron’s Funds remain open, which means that as long as the SpaceX mark within BARAX and BGAFX has not shifted higher since March 31st, you can buy into the Mutual Funds and essentially have a large chunk of your investment allocated to SpaceX at an implied $1.25 Trillion valuation just days before the company is expected to IPO at a $1.75 Trillion valuation.

Assuming the AUM of BARAX and BGAFX has remained unchanged since April 30th, BARAX could experience a NAV uplift of 10% if SpaceX closes at a $1.8 Trillion valuation, and 14% if SpaceX closes at a $2.0 Trillion valuation, and BGAFX could experience a NAV uplift of 7% at $1.8 Trillion, and 10% at $2.0 Trillion. Even if the funds have doubled in AUM since, as long as the SpaceX mark has not increased, there is still potential for a helpful NAV uplift next week when SpaceX goes public.

This trade goes right back to the saying “too many cooks spoil the pot”.

Investors in these funds have long awaited the payday of the SpaceX investment, but because the funds are not closed, new investors can swoop in, establish SpaceX exposure at a lower-than-IPO valuation, and dilute the existing investors’ potential profits, thus “spoiling the pot” and siphoning some of the windfall.

Unfortunately, the NAV uplift trade is quickly getting out of the bag.

Bloomberg wrote an article about the expected NAV uplift yesterday, and Retail investors have plowed $1.1 Billion into the Baron First Principles ETF after realizing 2% of it is allocated to SpaceX.

While the Mutual Funds have barely been discussed, I think it is only a matter of time before the opportunity is discovered by the same crowd piling into the ETF.

While an investment in these Mutual Funds may provide the opportunity to guarantee yourself some SpaceX exposure, there are also several risks.

First of all, it is impossible to determine what percentage of the funds are invested in SpaceX. As with huge inflows into the Baron First Principles ETF, if BARAX ($3.3 Billion AUM as of March 31st) or BGAFX ($839 Million AUM as of March 31st) experience inflows (perhaps they doubled in size) the weight of SpaceX could become significantly diluted, reducing potential NAV uplifts.

Secondly, it is possible that Baron Funds has increased its mark for SpaceX in NAV calculations (implying you are no longer getting exposure to SpaceX at a $1.25 Trillion valuation). Looking at recent performance, there was a bump in BGAFX that I believe was caused by its exposure to Semiconductors, but there has been no recent bump in BARAX, leading me to believe BARAX has not increased the mark of its SpaceX position, which is why I find it the more attractive of the two.

Additionally, BARAX has substantial equity investments in the broader market, meaning that an investment in the fund leaves you exposed to general market risk on top of SpaceX, which is not guaranteed to go public, and may not be well received by the market.

Importantly, unlike ETFs, there are no limit orders for Mutual Funds. If you create a subscription to purchase $100,000, you don’t know the NAV you are purchasing at until it is calculated after the market close and your order has already been filled. In practice, this isn’t generally an issue, but it does leave you exposed if Baron Funds decides to suddenly mark up the value of its SpaceX stake, or chooses to not immediately update the NAV when SpaceX goes public next week.

Finally, brokers such as Schwab and Fidelity may impose a $49 fee for selling a Mutual Fund if held for less than 90 days, adding transaction costs. It’s also possible that BARAX or BGAFX modifies its redemption fee to disincentivize flippers. Currently, there is no load or redemption fee on both BARAX and BGAFX, but that can always change.

Despite these risks, I find the setup for BARAX attractive given the SpaceX exposure and potential NAV uplift, and have allocated 1% of my Portfolio to it. Even if the fund has experienced significant inflows (diluting the SpaceX stake as a percentage of NAV), an investment still represents an opportunity to lock-in pre-IPO exposure to SpaceX at what might still be a sub-IPO valuation (assuming the mark has not moved).

While you could wait until next week to establish a position closer to the actual IPO, I think there is a possibility BARAX closes itself to new investors to preserve a potential SpaceX windfall, hence why I initiated my position this week.

This trade isn’t risk free, but if the SpaceX mark within BARAX is still $1.25 Trillion and the IPO is successful, I think the trade has potential and I will attempt to cash out my shares shortly after the IPO. Given how many moving pieces there are to this trade and the general market exposure present in BARAX, I think it makes sense to size conservatively.

Keep this one on the down low, too many cooks spoil the pot.