April 2026 Portfolio Review

Hunting Global Value - Japanese Healthcare, European Logistics, and a Capital-Light Net-Net - Here's What I've Been Buying

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

What is it worth to you?

That’s a question I think of often when it comes to AI. In both markets and in real life, everything is relative. You buy a stock when you think it’s worth more than what it’s trading for, you buy a preferred when the risk adjusted yield in excess of what you might earn in cash, you buy a product when the value it provides to you exceeds the price; the larger the differential, the happier you are to do it, and the more you want of it.

Over the past couple of weeks, we’ve seen countless complaints on Twitter and tech news from angry customers asserting Claude has “dumbed down” its models or ChatGPT was throttling usage. While many were quick to jump on the companies and assert they were doing this because the business model was unprofitable, I see it differently: the complaining highlights how large the value differential is.

A junior software developer (at least in the US) might cost $75,000 - $150,000, and I think most would agree Codex or Claude Code is akin to having a developer on call 24/7. AI serves as a personal butler when it comes to researching, finding restaurants, maybe even locating cheap laptop deals. It’s not perfect, but things are moving quickly. With that in mind, the price of a $100 Claude Max or ChatGPT Pro plan is actually a bargain to power users. When a $100 plan gets throttled, users riot because they are losing way more than $100 in value.

Even if the labs hiked pricing to $500 or $1,000 a month, it would still be a bargain to the power users driving AI demand. The price of a token to a company using AI to handle things like phone support or data entry is still significantly underpriced.

This isn’t a mere anecdotal observation, the proof is in insatiable demand. Anthropic’s ARR has surged to $30 Billion from $9 Billion in just 3 and a half months. Nebius (a leading neocloud) is sold out of capacity. Rental Rates for older H100 Chips are up significantly, and in fact have risen since 2024. It doesn’t seem like things are slowing down at all.

My point is, the value AI brings to the table far exceeds the cost, and with that in mind it’s easy to see why the Hyperscalers and Frontier AI Labs alike are clamoring for more chips: the value of the chips, to them, significantly exceeds the price, and the value of the “tokens” they provide to their clients also significantly exceeds the cost. As long as that is the case, I think the AI trade has legs, and that AI adoption will continue accelerating.

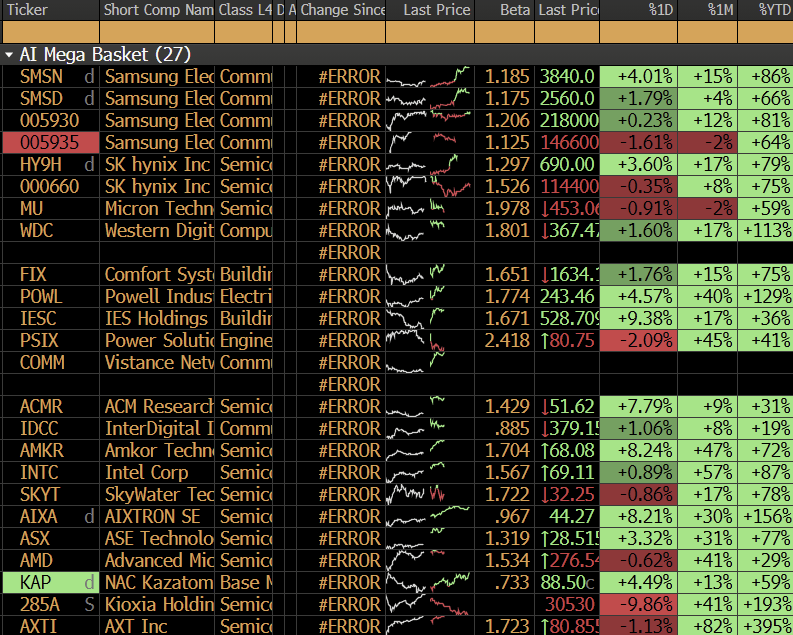

The AI Megabasket I posted earlier this year has been a major driver of returns in my portfolio. I’ve made a few adjustments, and have cut several of the more speculative names. My Memory and Storage portfolio is just SK Hynix, Samsung, Western Digital, Micron, and Kioxia (in that order), and my Infrastructure basket is comprised of IES Holdings, Comfort Systems, and Powell Industries.

Has my portfolio been fully “AI Pilled”? A bit, but I also see a lot of value in inexpensive banking, insurance, and discount-to-nav situations with aligned management teams and aggressive capital allocation plans to address the discount.

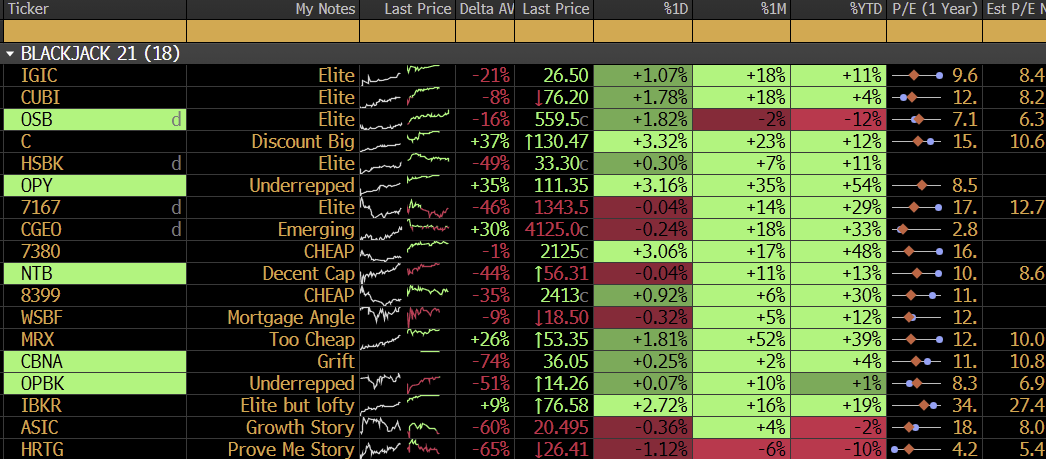

The “Blackjack 21” index continues to set All Time Highs and is up 16.4% YTD on an equal-weight basis. While it might not seem like much next to the AI names, it is significantly ahead of the MSCI Global Financials Index (-0.83%), the S&P 500 Financials Index (-5.20%). I think components in this basket still have significant tailwinds: Japanese banks are poised to gain from rising yields, and the aggressive capital allocation of Halyk Savings Bank, NT Butterfield, Georgia Capital, and International General Insurance continue to drive returns and improve ROE.

Before I get into the list of all 45 Portfolio holdings, I wanted to discuss the significant opportunity Global Value presents. The MSCI EAFE and MSCI Emerging Indexes are finally putting on a show after more than a decade of significant underperformance relative to US Equities.

While some of the reversion is due to Korean Equities (which is almost purely an AI trade), I think there is a long-term tailwind from improving global capital allocation and the “Americanization” of foreign equities. Japan, Korea, China, and the EU are putting increasing amounts of focus on corporate capital allocation. Japanese companies who used to rewards shareholders with “Yutai” (gifts such as discount cards and food) have pivoted to share repurchases, and management teams have aspirational Price to Book Ratios, European companies (who were previously allergic to anything other than a mediocre dividend) are wading their way into buybacks. The bottom line is these companies are finally being run for the benefit of the shareholders.

While the broader indexes have surged as a result, however, many small cap names with improving fundamentals and shareholder friendly capital allocation have been entirely left behind due to their lower liquidity and limited Institutional interest.

I think these setups are exactly where retail investors have an edge: finding companies with strong capital allocation, aligned management teams, and inflecting fundamentals that are simply too small for larger investors to touch. If you think about it, the liquidity discount does make sense. If you are a large Institutional Investor looking at two identical companies at the same valuation, but one has $1 Million in ADV while the other has $10 Million in ADV, you’ll of course opt for the more liquid investment. Over time, however, I think you can generate significantly higher returns by exploiting this phenomenon and positioning yourself in names at a valuation discount that have aggressive capital allocation plans in place to close the gap.

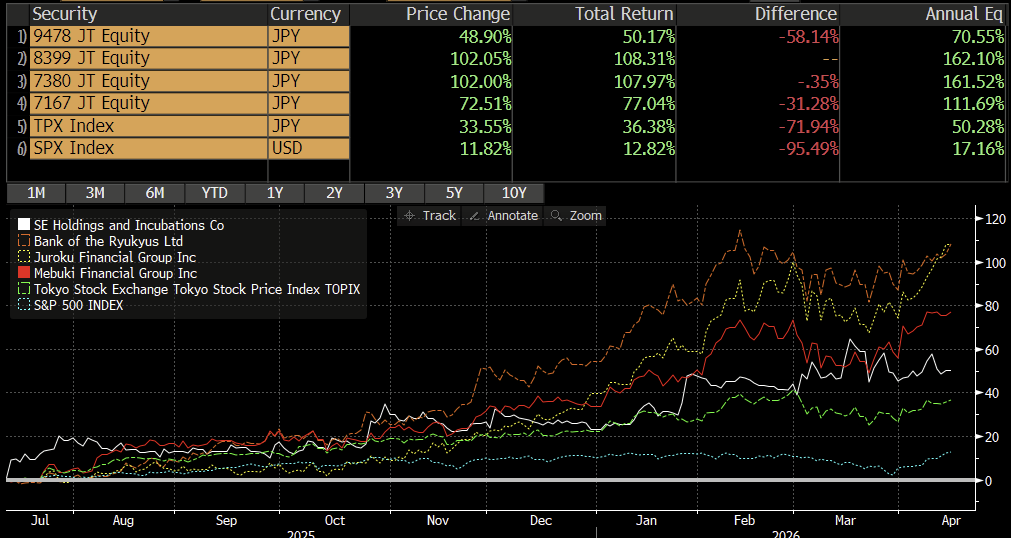

I haven’t pitched Japanese Equities since last summer. All four Japanese picks have significantly outperformed the broader index as well as the S&P, and astoundingly, three out of four have further 30-60% upside to Tangible Book Value.

After spending a lot of time screening, I’ve found two new Japanese companies with a similar setup, as well as three other value names that I believe are wrongly discounted. Before we get into the existing portfolio, here are the new positions.

Trade 1: “Buy a Pile of Cash, Get a Business, Free”

Long MOMO US Equity

Sector: Technology

Conviction: Medium

Current Price: $6.29

End of Year Target: $7.00

Forward P/E: 6.5x

Price / Tangible Book Value: 0.66x

Price / Adjusted Tangible Book Value: 0.90x

Shareholder Return Yield: 16.4% (Dividend: 4.7%, Share Repurchases: 11.7%)

Hello Group (MOMO US) is a Chinese social media company operating two flagship apps: Momo, a social networking and live streaming platform, and Tantan, a dating app commonly considered to be the Chinese version of Tinder. Momo’s domestic Chinese business has been in a steady decline, paying users have plummeted from a peak of 9 Million to just 3.5 Million driven by competition from Douyin (Chinese TikTok) and a years long crackdown on underreporting of tipping and gift income earned by livestreamers.

Momo stock is down nearly 90% from its 2017 Peak of $50 and seemingly prices in imminent implosion, but I think there is more to the story here. Momo’s Q4 2025 report just a few weeks ago showed the situation is inflecting: Chinese paying users have stabilized after an all time low of 3.5 Million in Q2 and climbed sequentially to 3.7 Million in Q3 and 3.9 Million in Q4, the first two consecutive quarters of growth since 2021. Additionally “overseas revenue” from Momo’s global portfolio (Happn – European Dating App, Soulchill – MENA Live Streaming Platform) has been accelerating. The International Portfolio of apps, which just a few years ago comprised just 1.6% of Revenue ($230 M RMB), now comprises 19.3% of Revenue ($2 B RMB) and have been guided as within striking distance of $3 B RMB in 2026:

“Something like RMB 3 billion in overseas revenue for 2026 is a pretty achievable target.” – Peng Hui – CFO, Q4 2025 Earnings Call

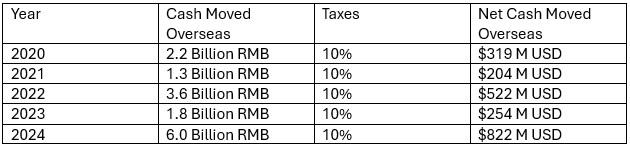

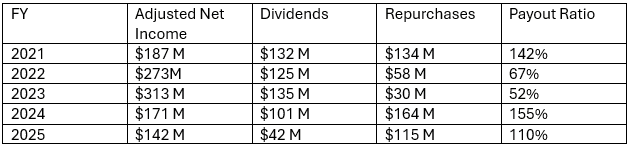

MOMO has always been viewed with wariness by American investors due to its VIE (Variable Interest Entity) structure, common among Chinese ADRs. MOMO itself does not own its Chinese operations, it instead has contractual economic rights to receive dividends from its Chinese business. Due to the VIE structure, significant cash (1.5 Billion RMB) is required to remain on the Mainland as “a statutory reserve”, and any dividends remitted to the overseas entity is assessed an additional 10% withholding tax on top of Corporate Income Taxes. While this setup isn’t optimal, Momo has routinely demonstrated excellent capital management and a willingness to move cash out of the Mainland to reward shareholders. Over the past 5 years, Momo has moved 11.4 Billion RMB (approximately $1.58 Billion USD) for use in share repurchases and dividends.

Much of the 2024 distribution was used to pay back bank loans at the parent level as well as a Tax Settlement for prior year taxes. Nevertheless, MOMO’s history of paying dividends to its parent entity is demonstrative that the cash profits generated in China are not trapped.

Additionally, since 2021 MOMO has been using cash paid offshore to reward the shareholders. In fact, MOMO has paid out more than 100% of adjusted net income in the form of repurchases and dividends 3 out of the last 5 years.

I think the capital return intensity is what differentiates MOMO from typical value traps. Anyone with a screener can find names at < 7x earnings, but how many of the names that show up return 100% of income, or even 50%, to the shareholders? Very few.

MOMO’s core business is capital light, and the balance sheet is comprised entirely of cold, hard cash. Essentially, MOMO shares are a pile of cash with a gushing app business on the side.

MOMO isn’t risk free, a sudden Chinese crackdown on VIE’s could ravage the company (as well as other VIE’s such as BABA, NIO, etc), although it is important to note MOMO’s Cayman Shell isn’t totally empty, the European and Japanese app portfolio is not subject to Chinese regulation. There is also the prospect of a continued Chinese crackdown on livestreaming and dating apps, which would significantly harm Momo and Tantan.

While this obvious downside exists, I also think there is significant upwards optionality. MOMO’s portfolio of International apps is rapidly growing, and much of the portfolio is not yet monetized which will provide a further tailwind once it is:

“We expect Yaahlan to turn profitable within this year, and Amar should be behind it by half a year or so. The AI-driven product in MiraiMind remains in investment mode as we prioritize user growth and product capability. We don’t want to focus too much on reaching profitability -- the ability for that product. But of course, for each of the region we are in, we also have a payback period that’s required.” – 2025 Q4 Earnings Call

MOMO currently trades at $6.29, a steep discount to its $7.50 net cash balance. Even if you strip out the $1.5 Billion RMB in “statutory reserves” MOMO is required to keep onshore (which I think you should since that cash earns interest but is otherwise locked up), MOMO still has a net cash position of $6.13 per share.

MOMO insiders, including CEO Yan Tang, own 30% of the company (currently worth $300 Million) and are highly incentivized to do the right thing given executive compensation of $6.3 Million USD is just a fraction of their ownership stake. Insider selling from RSU’s has averaged < $10 Million a year, a minimal amount relative to both ownership and the company’s sizeable repurchases.

Simply put, at $6.29 a share, you are getting $6.13 in cash a share, along with an International portfolio of cash cow apps run by aligned insiders at a 100% payout ratio, for just a few cents. It doesn’t get more deep value than that.

MOMO has historically been very active in repurchasing shares in the $6 - $7 a share range (they repurchased 16.8 Million shares in 2025 at $6.84 a share), and I think they are likely to be even more aggressive in the $5 - $6 range, which creates a compelling setup if you are looking for a short-term trade. Of course, Dating Apps and AI Companions will never be seen as a “premium” or “quality” business, so I am not expecting it to trade at 10x or 15x earnings, but even a small re-rate to 8x earnings would imply $7.71 a share, significant upside from the current price and still just 1.25x MOMO’s cash pile (and below Tangible Book Value of $9.75). With all things China, it makes sense to approach your sizing conservatively (< 2.5%), but at the current valuation I believe the market is ascribing MOMO’s app portfolio zero value, and that it is worth considering a starter position at these prices.