Global Dental Labs and US Malls

Updates on Two High Conviction Trades: Modern Dental Group and CBL Properties

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

Quick updates on two high conviction names: Modern Dental Group (3600 HK) and CBL Properties (CBL US).

Modern Dental Group (3600 HK)

2025 P/E: 8.9x

2026 Forward P/E: 8.4x

Dividend Yield: 3.45%

Insider Ownership: 67%

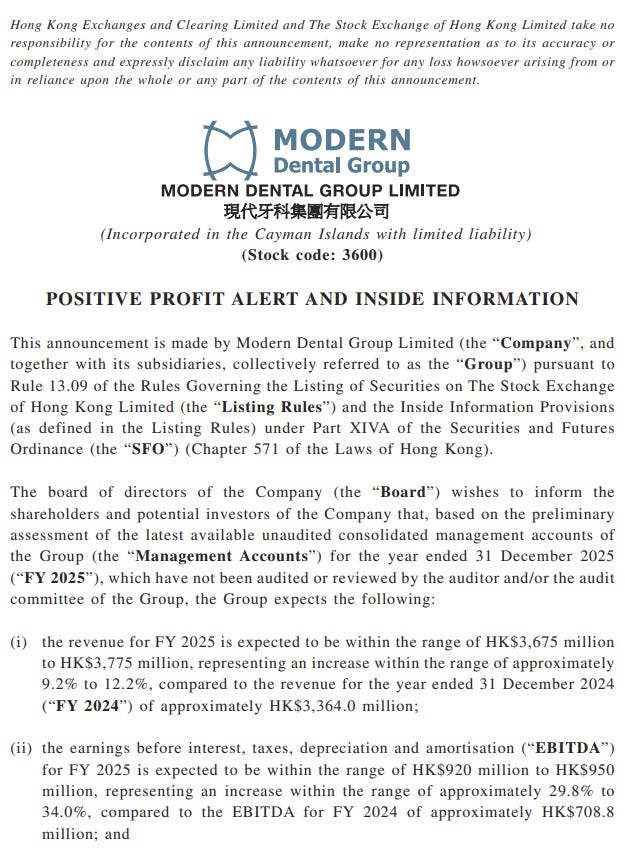

Modern Dental Group released a positive profit alert last night, indicating 2025 Net Income surged to $600 Million HKD, a 48% increase over 2024’s $406 Million HKD.

I said it in the recent Trade Review and I’ll say it again: Modern Dental is one of my favorite HK Small Caps.

Modern Dental Group (3600 HK) is a global dental prosthetics (crowns, bridges, dentures, implant components, and aligners) manufacturer listed in Hong Kong, but its largest markets are Europe (48%) and North America (22%) where it operates 80 dental labs under local banners. It’s innovative approach of rolling-up local dental labs and inserting its offerings has enabled it to grow like a weed: it slashes overhead, reduces product costs, and increases distribution while avoiding a “made in China” stigma since the labs operate under local banners.

I believe Modern Dental Group trades at a deep discount to its intrinsic value due to lower liquidity and Western wariness over HK Small Caps - all too often “too good to be true” stories in Hong Kong turn out to be shams, casting a dark cloud and disbelief over many value setups.

Modern Dental Group, with its strong M&A track record, shareholder-first capital allocation (share repurchases in the 3-4 range, 2025 Dividend: $0.199 HKD, 2024 Dividend: $0.17 HKD, 2023 Dividend: $0.104 HKD), and significant insider ownership (67%), however, continues to shine through. The stock is up nearly 120% over the last three years as the good times roll, and Hillhouse Investment Management (an Asian investment firm with $60 Billion in AUM and a specialty in Healthcare Investments) recently acquired a 17% stake at $5.80 HKD from the founding Ngai family, signifying rare Institutional interest in a HK Small Cap. I believe Hillhouse’s January purchase marked a turning point: Modern Dental Group is now a value setup that is compelling enough for Institutions to buy-in at a premium.

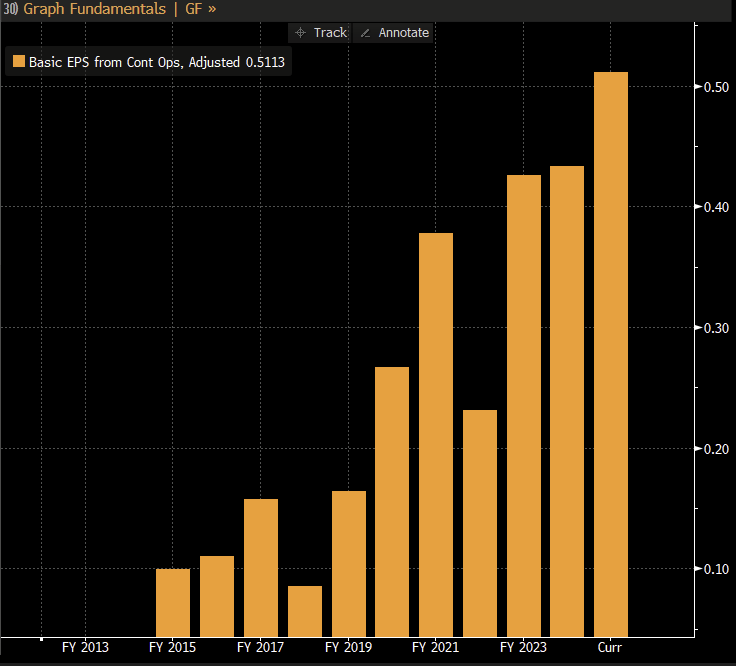

The positive profit alert is a welcome surprise. It affirms Modern Dental Group is already generating significant returns from its acquisition of Hexa Ceram (Thailand), and Digital Sleep Design (Australia), both of which closed in 2025, and the company is likely to report earnings of $0.64 HKD for 2025 (a CAGR of 19.25% over the last decade) and a bump in the dividend when the Board of Directors convenes later this month.

As the company continues to grow, attracts Institutional attention, and returns cash to the shareholders, I think Modern Dental Group will prove that the “HK Discount” applied is unwarranted: if it were listed in the US or EU it would likely demand a much higher valuation. Based on the positive profit alert and estimating moderate growth of 5-7% in 2026, I believe Modern Dental Group shares are within striking distance of $6.50 HKD - $7.80 HKD, which still implies a very reasonable multiple of 10x - 12x for a business with its track record of expansion.

CBL Properties (CBL US)

2025 P/FFO: 5.8x

2026 Estimated P/FFO: 5.6x

Dividend Yield: 4.76%

Insider Ownership: 30%

CBL Properties, an operator of lower-tier Malls and Open-Air Centers, announced a transformative financing package last Thursday that blows a hole through the “bear case”. For years, CBL detractors have asserted the company deserves a low valuation due to the “music stopping” in 2027 when CBL’s sizeable Term Loan matures. It was a reasonable concern to have, no-one wants to own a melting ice cube and if CBL wasn’t able to successfully re-finance, it’d have to hand over the keys on more than a dozen properties that accounted for 25% of FFO.

After last weeks refinancing, however, those concerns have been put to bed. CBL refinanced its $634 Million 2027 Term Loan with two smaller packages, a $425 Million Non-Recourse Term Loan secured by 13 properties (7.40%, Matures in 2031), and a $176 Million Non-Recourse Mortgage secured by 3 open-air centers and one mall (SOFR + 4.10%, Interest-Only, Matures in 2031 with two optional one-year extensions). While the loans carry a slightly higher weighted average interest rate of 7.50% vs 6.42% on the previous Term Loan, the package is massively accretive to cash flow.

How? Now that CBL is on much more solid financial footing, lenders are willing to accept significantly lower amortization: the $425 Million Term Loan is amortizing on a 22.5 year schedule, and the $176 Million Mortgage Loan is interest only. As a result of significantly decreased debt paydown, CBL’s 2026 guide for principal amortization has dropped from $90 - $95 Million to $58 - $63 Million, implying an additional $32 Million in discretionary cash flow. Even after accounting for $4 Million in additional Interest Expense, the net impact to CBL is an extra $28 Million in Discretionary Cash Flow, a massive 42% increase to 2025’s $66 Million in Discretionary Cash Flow.

Simply put, CBL’s financial engineering pushes out the “debt wall” 5 years and sacrifices just $0.18 out of its $6.90 in Funds From Operation (due to $4 Million in additional Interest Expense) to boost Discretionary Cash Flow from $66 Million to $94 Million. When your stock is trading at just 5.50x Funds From Operation, incurring $4 Million in Interest Expense to free up $28 Million for dividends and buybacks is exactly what you should be doing.

CBL is no stranger to capital returns, in 2025 the company returned $75 Million ($2.50 per share) via dividends and $18 Million ($0.60 per share) via share repurchases on roughly $66 Million of Discretionary Cash Flow. With 2026 Discretionary Cash Flow likely to come in near $94 Million, CBL has plenty of additional firepower to raise the dividend and repurchase shares.

It’s important to note that (just like the previous Term Loan), CBL’s new Term Loan and Mortgage are entirely non-recourse - the company can simply walk away from bad assets if mall Real Estate plummets. Additionally, all collateral pledged for the new Term Loan and Mortgage already served as collateral for the previous Term Loan (meaning CBL did not have to add collateral), and in fact, the Northgate Mall in Chattanooga, TN was released as collateral, offering CBL flexibility to sell or borrow against this property.

Despite the progress CBL has made in delevering the balance sheet, pushing out the “debt wall”, and boosting Discretionary Cash Flow (not to mention 2025’s copious dividends and repurchases), the stock still trades at a massive discount to Simon Property Group, Macerich, and Tanger. While these peers clearly have higher class properties, the discount is astounding: even highly distressed entities trade at a more respectable FFO multiple (and they aren’t even repurchasing shares or paying a dividend). I am by no means calling for CBL to trade at 12x FFO or 8x FFO, but even a small bump to 6x - 7x FFO implies $44 a share at the midpoint, significant upside from the current $38 price.

Given the company was repurchasing shares around $35.62 in December, I think $37.50 (5% above their repurchase price) represents an attractive entry. CBL will likely never trade at a peer multiple due to its past history of implosion (this time I think things are different - the balance sheet is 98% non-recourse) and lower quality properties, but I think the elimination of the bear case, improving sentiment surrounding retail Real Estate, and a massive decrease in debt-paydown due to the refinancing package offers a compelling-setup at the current valuation. As long as CBL continues to return cash to shareholders, gradually delever, and maintain a non-recourse balance sheet, I think the setup will continue to work.

There is no need to subscribe, there is nothing below the paywall.