March 2026 Trade Review

Trade Recap - Here's What I've Been Buying and Selling

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

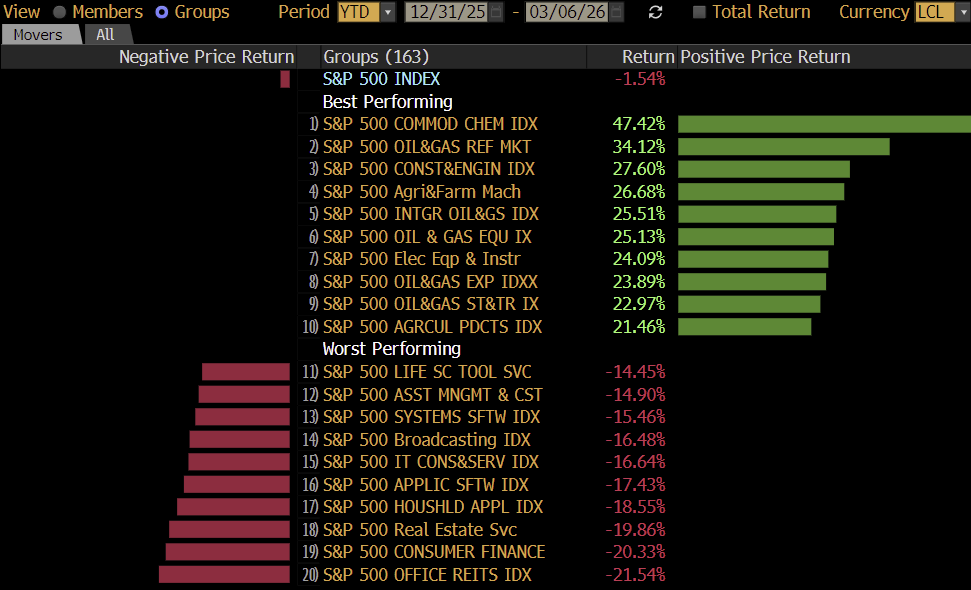

The S&P is down 1.34% YTD, practically unchanged. After a 25.95% SPX return in 2023, 25.00% in 2024, and 17.86% in 2025, this should feel like nothing, but Fintwit seems to be singing a different tune. To their credit, things really do feel different.

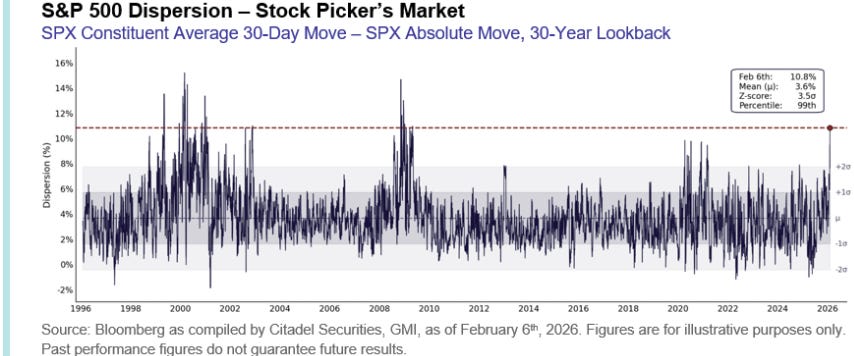

Underneath the headline -1.34% figure, whipsaw and dispersion are at the highest levels since 2008.

The whipsaw isn’t even limited to sector-vs-sector, sub-sector volatility is also raging. As an example, the broader Real Estate Index is up 6.29% yet Office REITs have plunged more than 21%. Financials are down 7%, yet Regional Banks were up nearly 14% at one point and are still clinging on to tiny YTD gains. To top it all off, traditionally sneered-at capital-intensive sectors such as Commodities, Chemicals, and Oil & Gas are leading the way with 30%+ returns.

Fund Flows are notably different. For the first time in years, QQQ inflows are flat while investors clamor into RSP (the Invesco Equal Weighted S&P ETF) and the Korea craze continues as investors remain undeterred by the largest drop since 2008.

While it is easy to blame these moves on the Iran War or Tariff Policy, most of them have been bubbling up since the beginning of the year and I think the widespread rotation and dispersion was bound to happen anyways.

The rose-colored glasses we had on for the last three years are coming off, and the AI bull case that powered a two-year “everyone is a winner” rally in everything aside from a few phone-support stocks (Five9, Concentrix, etc) seems to be increasingly two-sided. These days, it seems one name’s AI Bull Case is another’s Bear Case.

Pieces such as Citrini's Global Intelligence Crisis have gone viral, and I think these thought exercises are valuable: the World is changing at a light-speed pace, and it’s worth questioning assumptions and asking “what if’s” to see if your thesis is still compelling.

Just this weekend, Bloomberg reported Stripe and Circle are racing to build their own payments systems for autonomous agents. I’m sure you’re skeptical, so am I. But also consider in 2022 AI was a gimmick that made pixelated videos of Will Smith eating spaghetti, and now in just a few sentences, you can draw up a lifelike-video with near Hollywood quality. Tools like Claude and Shortcut can save minutes, even hours in Excel. Claude Code and Codex aren’t perfect, but they can turn one man into a one man army.

Just imagine where things are in a few years.

If Visa, Mastercard, and Amex are unwilling to let their payments systems be used for autonomous transactions (due to concerns over chargebacks or fraud), someone will create a system that will. In 5, maybe 10 years, you might forget to buy Valentine’s day chocolates and flowers, and perhaps you can load a Claude or OpenAI “Wallet” with 100 USDC or PYUSD (PayPal’s stablecoin) and simply tell it what you want it and where it should be delivered. Is this a certainty? Of course not. But there is a slim chance it happens, and the disruption risk it represents is easy to understand when many names trade at historical valuation highs and shareholders emphatically claim “it won’t happen”.

As an aside, even after Amex’s 20% December - March drawdown, Amex still trades at just a 2% discount to the 5-Year historical valuation average.

I’m the last guy to call a top, and in fact, I’m not going to. But from a stock-picker’s perspective, I think 2026 is shaping up to be fundamentally different: the playbook of piling into large-cap “quality” regardless of the multiple is no longer working, and I think this is when active management and conservative position sizing (keeping names below 10%) begins to shine, especially when it comes to steering clear of value traps such as troubled Software Oriented BDCs, no matter how cheap they appear.

Since I’ve started this blog, I’ve covered about 50 different trades, most of which are still open, across Financials (Banking and Insurance), AI Infrastructure and Memory, and Global Equities. Over the past two weeks, I’ve been making many adjustments to my portfolio: I’ve entirely closed a few winners, been stopped out on a loser, raised cash to 20%, and added 2 new names where I think the risk-to-reward is compelling despite the current turmoil.

To be entirely transparent with you, my Portfolio is heavily skewed towards Small Cap Value and International Equities. The S&P Regional Bank Index has a market cap of less than $600 Billion (a tiny fraction of the S&P 500’s $59.94 Trillion), and countries such as Sweden, Japan, Australia, Georgia, Canada, and Kazakhstan make up less than 10% of the World’s Market Cap, but a much larger portion of my Portfolio.

As a result, in this Trade Review I’m going to cover the trades I am in, what I’ve been trimming, what I’ve been adding to, and my conviction on each trade, but ultimately the weights are up to you to determine. I want this blog to be a place to see ideas and setups you might not usually see, when I write up Small Cap setups such as International General Insurance, CBL Properties, Chain Bridge Bancorp, and Georgia Capital, it’s to get these names on your radar. It’s entirely up to you to conduct your own due-diligence, determine if you find the thesis attractive, whether these trades are suitable for your portfolio, and of course what the appropriate weight might be.

The Trade Review is organized into:

Trade List and Performance Review

Trade History - Removals and Hedging

Trade History - Additions and New Positions

General Commentary and Conclusion