Opening the Gates

IBKR Adds Korea - Hynix at a 45% Discount, a Bank at Half Book, and a Valve Maker Flush With Cash

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

Who would’ve thought?

After years of anticipation, IBKR finally did it. As of last night, Interactive Brokers finally enabled trading for the last bastion of value stocks, Korean Equities.

Up until 2024, Korean markets were a graveyard for Western value investors. Corporate giants (“Chaebols”) would flood the market with listed subsidiaries who were carved up, spun off, and folded back in on terms that conveniently benefited the founding family at the expense of foreign investors.

Luckily, that has all begun to change as the wave of Asian financialization continues. Japan spearheaded the way in 2022-2024 via numerous market reforms, in particular the Tokyo Stock Exchange’s name-and-shame approach which requires companies at a low P/B ratio to disclose concrete steps on how to narrow the discount and improve ROE. Japan’s efforts were wildly successful, and Korea was eager to replicate the same for itself. Lee Jae-Myung, the governor of Gyeonggi, ran for the Presidency in 2025 on a pledge to eliminate the Korea discount and to double the Kospi Index (since his inauguration on June 5th, 2025, the Kospi is up 136%).

While much of Korea’s red-hot market is ascribable to the performance of SK Hynix and Samsung Electronics, I think there are also significant regulatory tailwinds behind Korean equities, such as the recent reduction in dividend tax from 45% to 15-30%, a 20% excess surtax on Chaebol retained earnings that aren’t distributed to shareholders or reinvested in the business, and fortifications in the Commercial Act (July 2025) that enable minority shareholders to fight unfair M&A. The bottom line is, Korea is rapidly transforming into a shareholder-friendly jurisdiction.

What I like about Korean Equities in 2026, similar to Japanese Equities in 2025, is that there are many straightforward value setups. This isn’t a matter of finding the next Nvidia, or stumbling upon the next “AI Bottleneck”. I’m not smart enough, anyways. I’m just looking to follow my framework and find value that already exists, and is simply being unlocked and returned to the shareholders via Dividends and Repurchases.

I think in Korea, where nearly half of listed equities trade at a sharp discount to Tangible Book Value (at least up until recently), this approach is likely to yield dozens of attractive setups. They won’t be home runs, but I think even a small allocation to a diversified basket of Korean value names has the potential to yield attractive returns, particularly as hungry value investors slowly pour into the country. I’ve had a couple names on my buying list for months, here are three value setups that have caught my eye.

1. SK Square - 402340

Price: 805,000 KRW

Sector: Technology

Price to Tangible Book: 0.56x

Implied P/E: 2.6x (Look-Thru Basis to SK Hynix)

Shareholder Return Yield: 0.5% (Solely Repurchases)

SK Square is an investment holding company that was spun off from SK Telecom in November 2021 to take direct ownership of SK Group's non telecom assets. Its consolidated operating businesses (ecommerce, music, and advertisements) generated 1.41 Trillion Won of revenue in 2025, but are not meaningful. SK Square’s real gem is its 20.07% stake in SK Hynix.

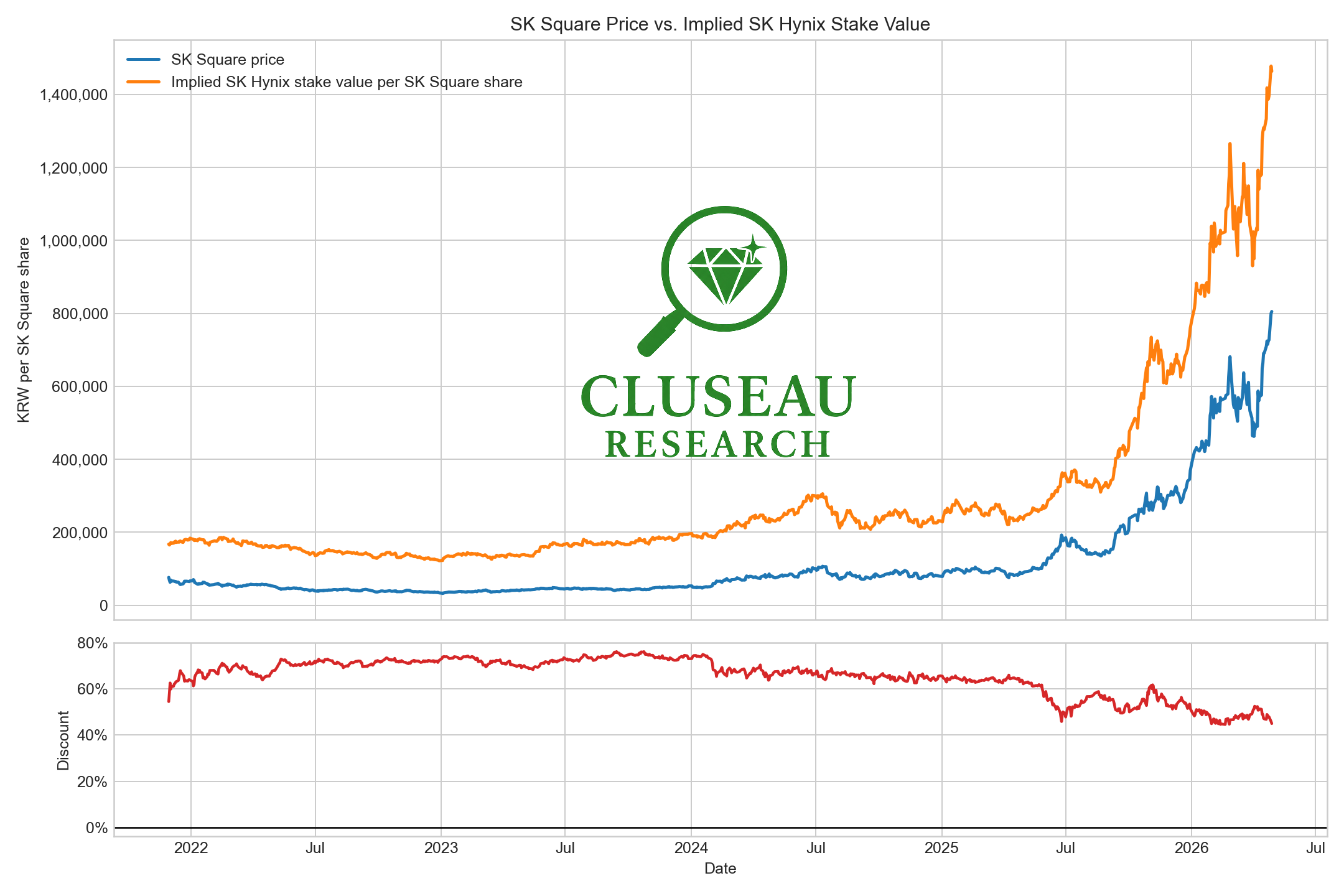

SK Hynix shares comprise 95% of SK Square’s assets, making SK Square a pure-play way to get exposure to SK Hynix at just 0.55x the mark-to-market value of the 20% SK Hynix Stake.

The management team of SK Square is acutely aware of the discount to Tangible Book SK Square is trading at, and has slowly reduced non-core holdings and used the proceeds to steadily reduce the share count from 141 Million in 2022 to 132 Million currently.

These shareholder-friendly steps have helped reduce the discount, and SK Square recently achieved its November 2024 goal of trading at 0.5x of NAV. The company has attracted several activist investors such as Dan Loeb, and announced an updated goal on March 25, 2026 of trading above 0.7x NAV by 2028. I think it’s clear the company is indicating “More repurchases are on the way”.

At just 0.55x Tangible Book Value with shareholder-friendly capital allocation, I think SK Square provides a unique opportunity to gain exposure to SK Hynix at an extremely attractive valuation (2.6x Hynix’s Forward Earnings on a “look through” basis). You could argue SK Hynix is already somewhat interesting around 4.8x forward earnings, but getting exposure at a 45% discount via SK Square seems to be an even more attractive opportunity, provided you are bullish on the memory trade.

Of course, there is tracking risk, there can be no guarantee the price of SK Square will track the value of its SK Hynix stake, but as shown in the graph above, the discount does seem to be closing and I think IBKR enabling Korean Equities will add additional momentum as value investors discover the opportunity. SK Square may constitute a PFIC (Passive Foreign Investment Company) under US Tax Law, which could pose adverse tax consequences to US Investors. As always, you should consult a qualified financial advisor and tax professional before making any investment decisions.

2. IM Financial Group - 139130

Price: 19,110 Won

Sector: Banking

Price / Tangible Book Value: 0.51x

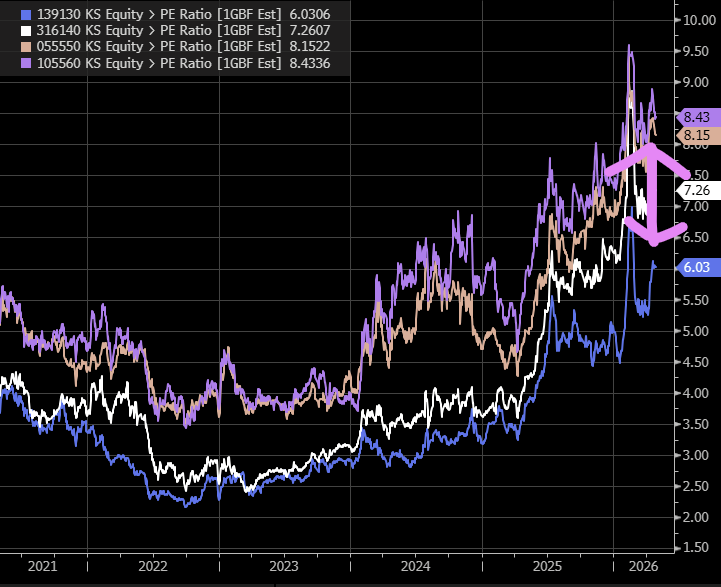

Forward P/E: 6.20x

Shareholder Return Yield: 6% (Dividends: 3.7%, Share Repurchases: 2.3%)

iM Financial Group, formerly DGB Financial Group, is the parent of iM Bank, a small Daegu-based bank that has recently become the first Korean regional bank promoted to nationwide commercial status in 30 years.

iM is a turnaround story. Over the last 3 years iM Bank has steadily grown its deposit base (expanding into Chungcheong, Gangwon, Honam, Jeju in 2024), significantly reduced bad loans, returned its Securities Division to its first year of profitability since 2022, as it embarked on its National expansion. iM’s impressive turnaround has attracted significant Institutional attention, several subsidiaries experienced credit rating upgrades in 2025, and iM Financial has become one of most “foreign-owned” banks in Korea. Currently, foreign investors hold 45% of shares outstanding, which is notably high for a Korean Regional Bank.

I believe there is a significant tailwind behind mid-sized Korean banks. High interest rates, stable credit quality, and rapidly improving capital allocation policies has driven a stampede into industry titans such as Woori, Shinhan, and KB, and I believe foreign investors are beginning to focus on smaller competitors that still have a national presence, such as iM.

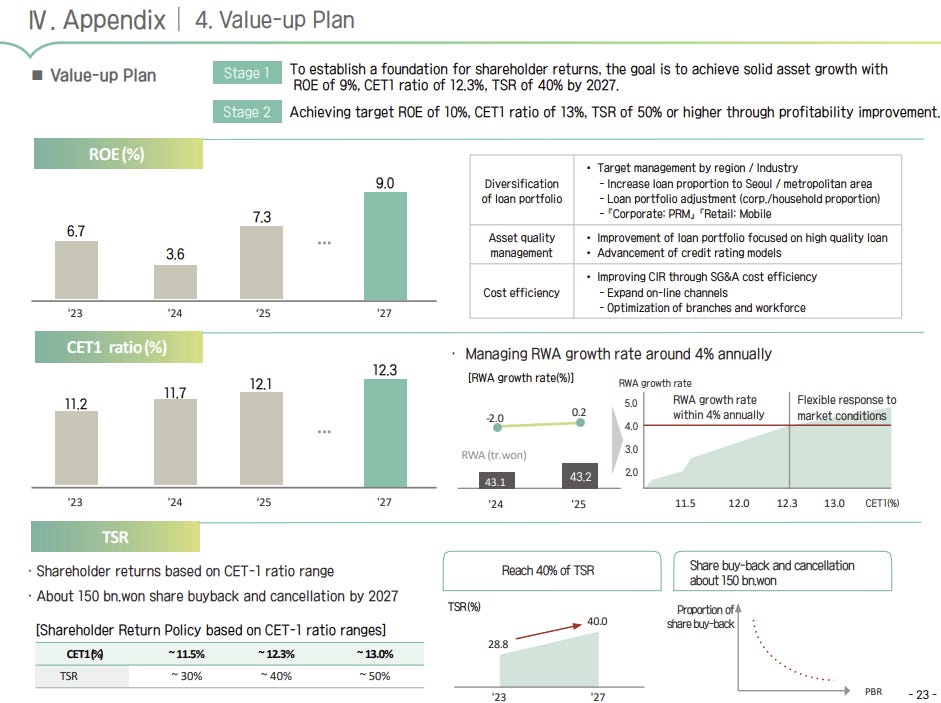

Now, iM is shifting its focus to shareholder returns. iM’s foreign-friendly investor disclosures, improving fundamentals, and capital allocation differentiate it from many peers who trade at similarly low multiples but do not return capital. iM’s “Value-Up” plan has set clear, attainable ROE and Capitalization Goals, and the company is making steady progress on its 150 Billion Won Buyback goal by 2027 (currently 50 Billion Won, 1.5% of shares outstanding, is remaining).

I think iM’s significant foreign ownership, a 10% stake held by competitor OK Financial (who purchased shares on the open market at just 6,000 Won in 2021, providing a strong vote of confidence amidst the turnaround), and continual insider buying from the management team is indicative that iM Financial is committed to transforming itself from a “value trap” into a well-run bank that earns its cost of capital.

At just half Tangible Book Value, 6x forward earnings, and with a 6% shareholder return yield comprised of dividends and buybacks, I think iM Financial represents one of the only remaining opportunities to ride the Korean Banking wave at a 6x multiple paired with strong capital allocation and significant foreign interest.