Boring Is Beautiful

Q1 Updates on Three Asian Value Setups

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

It’s been a busy earnings season and I wanted to share a brief update on two existing value positions that delivered excellent earnings, as well as a new position in Korea.

1. For Startups (7089 JT Equity)

I featured For Startups as a new position in the April 2026 Portfolio Review as Idea 3, "Capital Light in Japan" (Entry Price: 1,224 Yen). For Startup’s Q1 Earnings report (released on Friday), was excellent, and I think its 30% top-line growth and significant guidance upgrade are likely to finally get it some attention. Before I get into the results, I want to briefly summarize the story.

For Startups is perhaps the most Japanese company you can imagine, a Venture Fund, a Database of startups, and a Headhunter all in one. What it truly represents, however, is a pure play way to ride the wave of exploding Japanese VC Activity in a capital-light vehicle.

For Startups has significant ties to leading Japanese VCs such as M3, Incubate Fund KK, Globis Capital Partners, Wil LLC, Strike Co, and Sparx Group (who are also shareholders in the company). For Startups specializes in placing C-level executives and technology employees across startups, and leverages its close ties to existing Japanese VCs and its proprietary startup database (Startup DB Japan) to identify companies in need of its services. The company also has a small co-invest portfolio that it invests alongside its VC clients, while the portfolio is not meaningful at 600 Million Yen (less than 10% of the market cap), the combination of its Startup DB, the co-invest portfolio, and its close ties to leading VCs has created a massive referral base: when VCs have portfolio companies that need to hire, they just call For Startups.

The company has been riding the wave of increasing startup activity in Japan, and earnings have steadily grown from 22 Yen in 2021 to 99 Yen in 2025, a CAGR of 45%. The CEO, Yuichiro Shimizu, has routinely highlighted he believes the shares are undervalued, and in addition to pulling 2027 guidance forward one year, the company repurchased 160,000 shares (roughly 4% of the float) in March.

For Startup’s incredible earnings report (released last Friday) has caught my eye. Revenue for the first quarter of 2026 was up a stunning 63% year over year, and earnings per share jumped 80% (to 55 Yen per share), demonstrating the company’s significant operating leverage and capital-light nature. Unlike many Japanese companies who trade at low multiples due to heavy investment needs to remain competitive and a general inability to return capital, For Startups is the exact opposite: its headhunting business is inherently capital-light, and the company continues to opportunistically pursue share repurchases while still generating 50% top-line growth.

The company’s investor presentation (which is astutely posted in English to attract US attention) has guided significant growth for 2026: revenue growth of 25%, and 145 Yen in Earnings per Share (38% growth).

(Source: Company Filings)

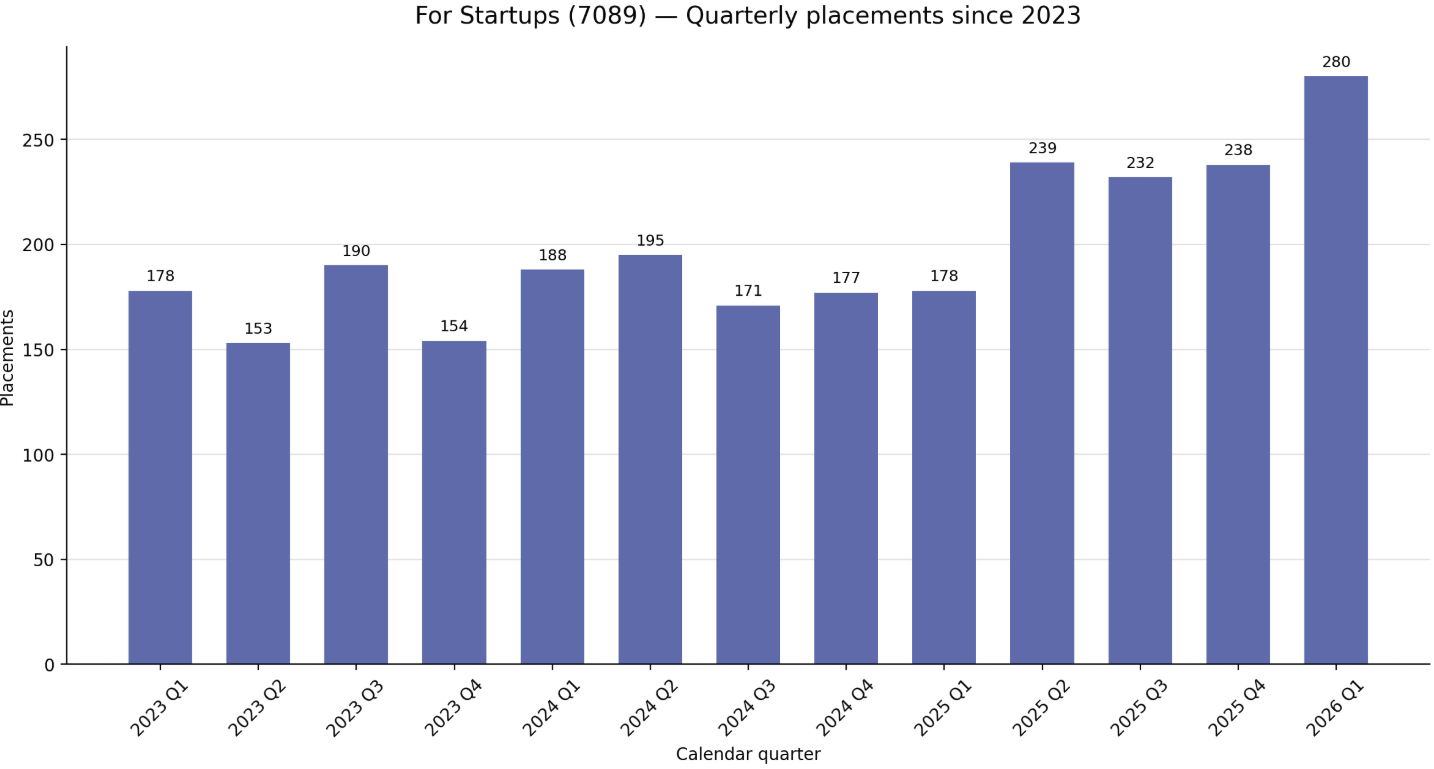

I think For Startups has all the markings of a “capital light compounder” aside from a migraine inducing multiple and the usual circle of GARP lovers who only get interested in 6% growth once it’s already trading at 30x earnings. I think the recent first quarter results and full year guidance upgrade to 145 Yen in EPS confirms the thesis I had last month: For Startups has positioned itself as an indispensable headhunter for the Japanese Startup industry, and will continue to ride the wave of elevated business investment. Quarterly headhunting placements are soaring, the company is increasingly focused on high ticket (salary) roles, and its Startup DB division is generating record annual recurring revenue.

For Startups excels in meeting my value investment criteria. The company specializes in catering to an under-served niche, has a clean balance sheet with a strong net cash position (approximately 330 Yen per share), has extremely aligned insiders who own 20% of the company, and is capital-light in nature, making it easy for the company to return cash to the shareholders.

With guidance for 145 Yen in earnings in 2026, I think the company is too cheap to ignore at 1,359 Yen, and that the combination of 30% guided earnings growth, a capital-light business, and the management team’s consistent history of execution, may warrant a 11x - 14x multiple, which would imply upside to 1,595 - 2,030 Yen a share.

The next two names are below a paywall for a very simple reason: both trade at deep discounts to Tangible Book Value, and are actively conducting highly accretive share repurchases. It’s a bit paradoxical, but the cheaper these stocks remain, the more value is created for long-term shareholders when management is able to repurchase stock at 5x earnings. If you have zero interest in Asian value investing, don’t subscribe. I can assure you both of these pitches are exceedingly boring, and you may even fall asleep at your desk if you read further.