Go Stub Yourself

Special Situations in Vistance Networks, Green Dot, and a Value Setup in OSB Group

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

Introduction

Stubs are some of my favorite asymmetric market setups. When a company disposes of major assets, many traders often “trim out” to lock in a quick profit, leaving behind a remaining business that nobody has spent time on valuing. In this piece, I’m covering two setups I believe the market has overlooked: the Aurora Networks stub within Vistance Networks, the new bank being formed by Green Dot and CommerceOne following Green Dot’s sale of its fintech assets, as well as a value bank, OSB Group, that doesn’t quite fit the theme but is simply too cheap to ignore at 6.3x forward earnings and 0.85x Tangible Book Value.

Vistance Networks (NASDAQ: VISN)

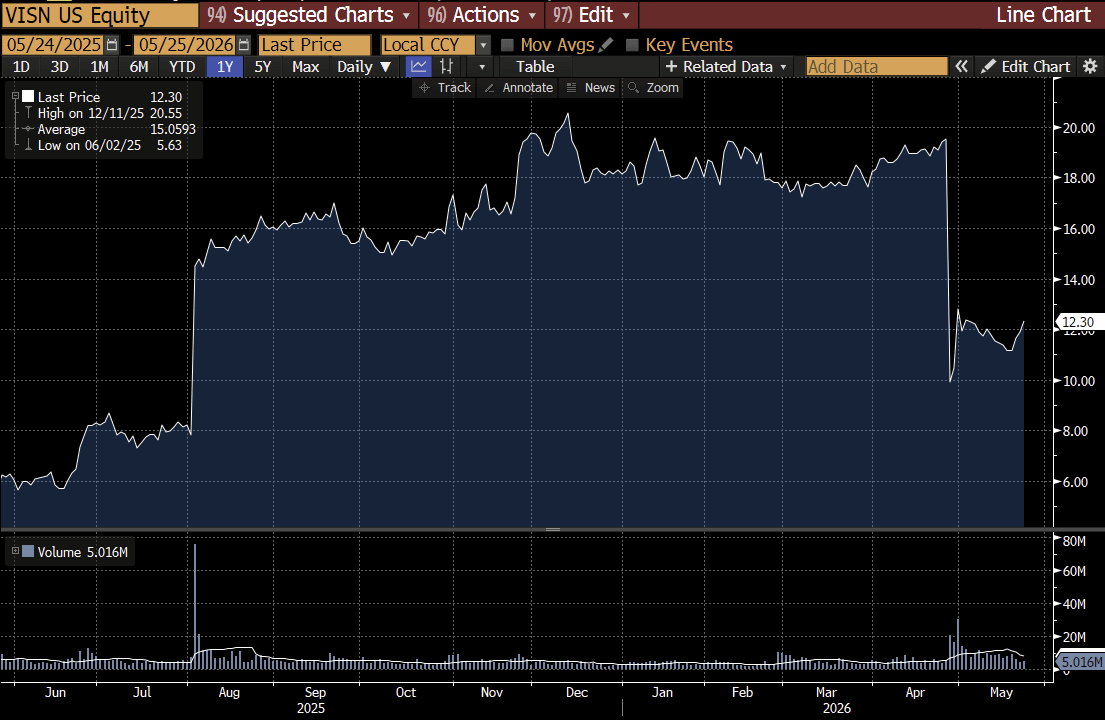

I’ve owned Vistance Networks (formerly known as Commscope) since 2024, and am extremely impressed with how the company has conducted itself. Over the past two years, Vistance has flipped the script and transformed itself from a debt-laden melting ice cube into an asset-disposition name focused on maximizing shareholder value.

In August 2025, Vistance announced a landmark sale, the $10.5 Billion disposition of its Connectivity and Cable Solutions segments to Amphenol. Vistance used the proceeds to entirely eliminate debt, redeemed all preferred equity, and recently used the remaining proceeds to fund a $10 a share special dividend. In April, Vistance announced another significant transaction, the sale of its Ruckus Networks Division to Belden Inc for $1.846 Billion.

After these two milestone sales, many assume Vistance is a shadow of its former self with insignificant remaining assets, but I see substantial value in the stub: it’s Aurora Networks division, who is poised to gain from the surprising comeback of coaxial cable.

Aurora Networks specializes in infrastructure broadband operators use to upgrade existing coaxial networks: headend and access platforms, DOCSIS 4.0 nodes and amplifiers, and virtualized access products. In simpler terms, Aurora sells the “upgrade kit” cable companies use to extract higher speeds out of their aging coaxial networks.

Recently, cable internet providers (such as Comcast) have come under immense pressure from expensive fiber buildouts by AT&T and Verizon (that offer significantly faster symmetrical upload and download speeds), and blazing fast over-the-air 5G Home Internet (offered primarily by T-Mobile).

The bottom line is cable internet providers have realized $99 a month for 50 mbps internet via their coaxial networks is no longer an attractive offering, and that they need to increase speeds and performance to keep clients from leaving. The Cablemagedon has transformed into an immense tailwind for Vistance’s Aurora Networks segment: cable companies are unwilling to commit to the massive capex of a fiber buildout (now that 5G Home Internet is rapidly taking market share) and instead want to get the most out of their existing coaxial networks via upgrades to the new DOCSIS 4.0 standard (delivery speeds up to 10 Gbps down and 6 Gbps up via coaxial cable).

Aurora Networks is one of the only fully integrated providers of DOCSIS 4.0 products, and a surge in DOCSIS upgrade interest from providers such as Comcast and Vodafone has resuscitated this seemingly dead segment back to life.

Aurora Networks Q1 revenue surged 32.6% to $298 Million and Q1 EBITDA jumped 31.7% to $50.3 Million, driven by record demand for amplifiers and nodes as well as new multi-year contract wins. The results lend credibility to the management team’s bullishness in the 2025 Q4 call, where they indicated large contract wins would drive 2026 results higher:

“Yes, I don’t think we’re going to give the precise number, but it’s a meaningful dollar amount. It’s tens of millions of dollars of opportunity that comes with that win.” - Kyle Lorenzten, CFO, in reference to winning new contracts

The point is, Vistance’s Aurora Networks segment isn’t a melting ice-cube. The backdrop is extremely favorable for 2026, 2027, and 2028, as these multi-year cable upgrades continue, yet the market is seemingly ascribing Aurora Networks very little value at Vistance’s current market price.

Vistance is currently sitting on $250 Million of cash (after paying out the $10 special dividend), and is primed to receive $1.7 Billion in net proceeds from the sale of Ruckus later this year. With pro-forma cash of $1.85 Billion, the implied valuation of the Aurora Networks segment is just 4.1x EBITDA, extremely low.

The company has indicated it intends to pay out “a significant portion of the excess cash” from the Ruckus sale and analysts have already modeled a $5 Special Dividend, so I don’t think Vistance is likely to become a value trap where a company has a lot of cash it refuses to return - instead, we are likely to see a sizeable special dividend and for analysts to increasingly focus on Aurora as the remaining entity.

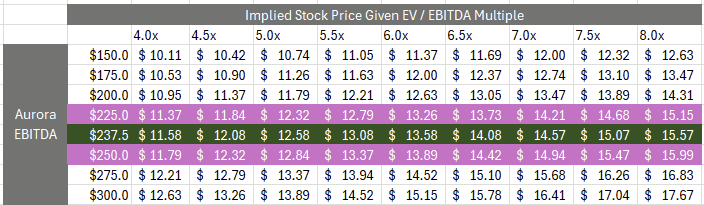

Bears have expressed concern about a lawsuit filed by lenders, who allege Vistance owes them at least $150 Million as a penalty for paying down debt early, but even if Vistance is found wholly liable for $150 Million (roughly $0.63 a share) it isn’t material to the story and the Aurora Networks stub would still be trading at an extremely inexpensive 4.7x EBITDA.

(The sensitivity table above errs on the side of caution and assumes Vistance will lose the $150 Million lender lawsuit)

Using management’s 2026 Aurora Networks EBITDA midpoint of $237.5 Million and an EV / EBITDA ratio of 6.0x, the implied share price of Vistance Networks is $13.58, representing upside of roughly 10% from the current price. Peers such as Harmonic Broadband (20x EV / EBITDA), Vecima (6.5x EV / EBITDA) and Teleste (8x EV / EBITDA) all trade at a significant premium to Aurora Network’s implied 4.7x EV / EBITDA multiple at $12.30 a share, which is surprising given Vistance’s multi-year contract wins from Vodafone and Comcast which serve as a testament to their superior offering.

I think you can make a strong case that the DOCSIS 4.0 upgrade cycle and increasingly attractive economics for upgrading coaxial in lieu of building fresh fiber will serve as a significant tailwind to Aurora Networks over the next several years. The Vistance management team has exhibited credibility, generated significant value for shareholders via asset dispositions, and recently announced a $100 Million share repurchase, which I believe is an excellent tool to utilize given the stub is trading at a steep discount to peers while the company is using no leverage (giving it significant flexibility to financially engineer the stock once the transaction with Belden is complete).

Vistance Networks isn’t risk free, the sale of Ruckus to Belden needs to pass regulatory scrutiny, and rising DDR4 memory prices are impacting Aurora Network’s margins. Still, the market is seemingly pricing Aurora Networks below < 5x EV / EBITDA, which I believe represents a rare opportunity to buy a “growth” name with a multi-year tailwind behind it at a deep-value multiple.

I’ve owned Vistance for years, and while I never like to chase, given the extremely attractive multiple the “stub” is trading for, Vistance has quickly become a high-conviction trade for me and I have been adding aggressively < $12.50 a share. Because the sale of Ruckus to Belden was announced just a few weeks ago, I think many traders simply haven’t realized how inexpensive the “stub” is, which would explain the sudden move down to $11 as traders took profits after the announcement, before the stock immediately recovered. I’m encouraged by significant increases in ownership from funds such as Carronade Capital (7.64 Million shares, +6.099 Million in Q1) and FourSixThree Capital (3.04 Million Shares, +1.055 Million in Q1), and I believe the market is slowly beginning to appreciate that there is more to the Vistance “stub” than appears at first glance. I am hopeful that as the market begins to treat Aurora Networks as a stand alone entity, the stock re-rates to $13.50 to $14.50 a share (which would imply 6.0x - 7.0x EV / EBITDA for the stub), and in the meantime, I think it’s worth considering an entry below $12, which implies just 4.5x EV / EBITDA at the midpoint estimate.

OSB Group (LSE:OSB)

Another name I have been adding to is OSB Group, an English bank specializing in “buy-to-let” (loans to landlords purchasing properties specifically to rent them out). I purchased OSB in March 2025 and it has certainly been a bumpy ride - the stock hit an all time high of 640p earlier this year, and has since tumbled to 500p as concerns over rising UK Interest Rates, a government crackdown on landlords, and general political instability mount.

These concerns have heavily impacted OSB’s shares, which are now trading at the steepest discount to Tangible Book Value since “Liberation Day”. What I like about OSB is that it is a “prove me” story: sentiment is routinely negative despite solid fundamental results, which continually provides the company an attractive window to return capital via accretive buybacks. The stock is currently trading at 502p (0.85x Tangible Book Value), 6.5x forward earnings, a 7% dividend yield, and importantly, OSB is repurchasing shares at the fastest pace on record.

Regulatory filings confirm OSB is rapidly deploying the 100 Million GBP buyback. The company has recently stepped up the pace to over 300,000 shares a day, nearly 0.08% of the float, and more than 30% of the daily volume. OSB is certainly making a statement with these aggressive repurchases.

OSB is well capitalized, their Q1 update indicates credit quality is stable, and I think OSB’s concentration in buy-to-let is in fact an underappreciated asset, as evidenced by larger UK Banks such as Natwest announcing new partnerships to muscle into buy-to-let. OSB has consistently generated a mid-teens ROE despite a high cost deposit base, which I believe makes it an attractive acquisition target for a larger peer with an inexpensive deposit base that who would want bolt on a specialist mortgage division without having to build an underwriting team and brokerage relationships from the ground up. A transaction makes even more sense when considering larger institutions all trade at a premium to Tangible Book Value, making it easier for them to use their shares as “currency” to take over OSB.

Until then, I believe OSB is attractive on a stand alone basis, and that recent drop provides a rare opportunity to enter a name that routinely exhibits shareholder friendly capital allocation and industry leading fundamentals, at a sizeable discount to its own Tangible Book Value.

The bear case is relatively straightforward: investors are concerned the retirement of longtime CEO Andy Golding signals trouble ahead, that UK yields continue to rise, that OSB is lending against overvalued collateral, and of course, that a nationwide rent freeze could slow demand for new mortgages and deteriorate the credit quality of existing ones. These concerns are sensible, but I think they are already priced into the stock and more importantly represent tail-risk scenarios rather than a plausible bear case.

What I mean by that is a nationwide rent freeze isn’t likely to happen, the UK 10 Year has already dropped 30 bps in the last couple of days as concerns over energy-incited inflation recede, the UK housing shortage is likely to persist (driving rents to fresh highs, benefiting landlords), and OSB’s Q1 update showed no signs of the credit issues investors fear. If anything, the setup has become unusually tilted to the upside: OSB is making steady progress towards its 2027 goals as it finishes technology upgrades, it is repurchasing huge quantities of shares below Tangible Book, and it has built enough excess capital to absorb a reasonable amount of housing weakness. At 0.85x Tangible Book, we don’t need the UK Housing Market to turn red hot for the setup to work, we simply need credit quality to remain stable and for the share count to continue expeditiously declining.

OSB is about 3% of my portfolio, and I continue to add steadily near 500p. Unfortunately, the company won’t be reporting earnings until early August, so it’ll be a while until the negative narrative can be firmly disposed of, but until then, OSB has 57.35 Million GBP remaining on its share repurchase program, which leaves it capacity to repurchase 200,000 shares a day until earnings (nearly 20% of the daily volume). As with all banks and insurers, we can’t ignore the left-tail risk of something going horribly wrong, which is why I think it makes sense to take a basket approach to these value setups and own several smaller positions rather than concentrating in one name. Nonetheless, I think OSB is trading at highly distressed levels despite solid fundamentals, a strong capital position, and ample capacity to return capital to shareholders. If you have an interest in adding value banks to your portfolio, I think OSB is certainly worth considering as a long-term setup. If inflation fears recede and yields decline, I believe OSB could quickly re-rate to 0.90x - 0.95x Tangible Book Value, which would imply 530p - 560p a share.

Green Dot Corporation (NASDAQ: GDOT)

I’ve initiated a small tracker position in Green Dot.

The Green Dot story is remarkably simple: the company is selling its non-bank fintech and payments assets to Smith Ventures, and merging its remaining bank assets with CommerceOne Bank (an affiliate of Smith Ventures, Bill Smith is on the board of CommerceOne). Upon consummation of the transaction, Green Dot shareholders are expected to receive $8.11 a share in cash, and 0.2215 shares of the new publicly traded bank. The question we need to figure out is what is the 0.2215 shares of the new bank worth?

The new banking entity has a seven-year MSA (Master Services Agreement) with the Green Dot Fintech platform, meaning nearly $4 Billion in relatively inexpensive, sticky, fintech deposits will be parked at the new bank until at least 2033. These deposits aren’t necessarily zero cost, the new bank will need to share about 40% of interest income with banking-as-a-service partners, but the positive of this MSA is that it ensures the new bank will hit the ground running with nearly $5.2 Billion in total deposits and just $750 Million in loans, providing ample room to grow.

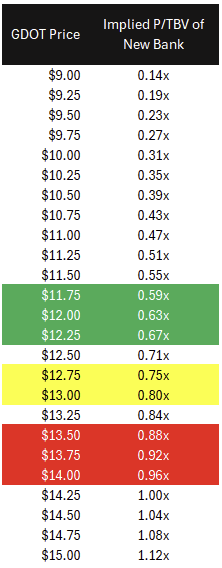

I’ll keep my analysis here brief: I don’t anticipate the new bank will trade below Tangible Book Value. The new bank will be extremely well capitalized, have minimal credit risk (despite recent charge offs at CommerceOne, the new bank will have an extremely low loan-to-deposit ratio which minimizes the impact of any credit deterioration in the existing book), and will have ample capacity to repurchase shares to engineer a 1.0x Price to Tangible Book Value ratio. With implied Tangible Book Value of around $27.80 a share for the bank, GDOT shareholders’ 0.2215 shares should be worth about $6.15 each.

Green Dot currently trades at $12.78, which implies the market is valuing the $6.15 value of the new banking stake at just 0.75x Tangible Book Value (this excludes the probability of the deal falling through, which is also likely priced in, but impossible to identify definitively). The below table shows the implied P/TBV of the new banking shares given the GDOT share price. As you can see, the risk-to-reward gets considerably more favorable in the high 11s and low 12s, which implies the new bank is being valued at less than 0.67x Tangible Book, extremely unusual for a bank with a clean slate and significant excess capital.

It’s important to note the transaction is awaiting regulatory approval, and the market will likely be apprehensive when valuing the new bank. Still, given the fact banking mergers are being approved at the fastest pace since 1990, I think the deal is unlikely to fall through, and furthermore, that the bank is likely to be valued at or above Tangible Book value given the company will have enough excess capital to simply repurchase shares until it is.

Even if the deal somehow falls through, I think Green Dot has a good chance of finding another suitor and is otherwise worth $9 to $10 standalone, which caps downside to about 25% from currently prices. Green Dot’s ownership list boasts value investors such as No Street GP (7.5% stake), Western Standard (6.26% stake), Steel Partners (2.2% stake - although it appears they are reducing their position), and M3F (1.3% stake), which makes me believe the combined bank is likely to hit the ground running with an immediate and attentive Institutional shareholder base.

The risk-to-reward for this setup varies significantly with slight movements in price, given what we are really trading here is the value of the banking stub. I’ve initiated a small starter position in Green Dot at $12.78, and have left a lot of dry powder to add in the low 12s and high 11s where the math becomes considerably more favorable and implies the bank is trading at less than 0.63x Tangible Book Value (under $12). I think it makes sense to keep Green Dot on your watchlists - any pullback not tied to a deterioration in CommerceOne credit quality or regulatory approval could offer a highly attractive entry point, especially as we near the listing of the new bank.

Conclusion

Of the three setups, I find Vistance the most attractive, followed by OSB. OSB’s steady capital returns and steep discount are notable, but ultimately it is likely constrained to Tangible Book Value (or a few percentage points higher), while Vistance’s Aurora Networks stub could significantly re-rate if investor excitement over the refurbishment of coaxial cable networks builds. As I write this, significant investor attention is being given to Harmonic and its Broadband Solutions segment, which I believe could benefit Vistance as investors realize there is more to the “stub” than initially meets the eye.

My blog isn’t intended to be a “clone a portfolio”. Instead, I want to cover and present niche setups, everything from Georgian Investment Firms to Samsung Preferred and SK Hynix, and ultimately, for you, the reader, to determine whether the setup is attractive and if it is appropriate for your Portfolio. My next Portfolio Review will come out mid-June, where I cover the 50 positions I hold and the setups I find most attractive to allocate new capital to. I hope you’ve enjoyed this piece, there is nothing below the paywall, I just can’t figure out how to send an email without one.