Sit Back, Relax, and the Enjoy the Dividends

Taking Advantage of the PFF Rebalance With Three 7% Preferreds

Disclaimer: By reading this article, you acknowledge and agree to the terms and conditions

I’ve covered a number of unusual setups: Asian Dental Labs and Japanese Regional Banks, Georgian Investment Firms, even Super PAC's Favorite Bank, to name a few. I’m not digging through obscure names for novelty, I do it because I believe the market is highly theme-focused and that as investors stampede from theme to theme, there’s value in examining what they’ve left behind.

One area I am increasingly finding value in is High Dividend Preferred Stocks, and not for the reason you’d expect. It’s not due to swinging yields or credit woes, rather, it’s due to Google, Microstrategy, and Supermicro.

What?

The connection between Google, Microstrategy, and Supermicro and High Dividend Preferred Stocks sounds like something you’d hear from an escaped insane asylum inmate, but allow me to explain. The world of Preferred Stock traders is extremely small and the $14 Billion iShares Preferred and Income Securities ETF (PFF) is a giant. As the ETF regularly rebalances, its 50k - 100k share trades leave a lingering impact on smaller Preferreds that may typically trade just 5,000 shares a day.

Microstrategy, Supermicro, and Google have been massive issuers of Convertible (Supermicro and Google) and Perpetual (Microstrategy) Preferreds, which are added to PFF’s benchmark, the ICE Exchange-Listed Preferred & Hybrid Securities Index. As these issuances continue, PFF is forced to match its benchmark and push out traditional bread-and-butter Preferred Holdings to make room for them. Essentially, Google, Supermicro, and Microstrategy are pushing traditional high-quality Preferreds out of the PFF ETF, and there are almost no active buyers to scoop them up. In my opinion, this indiscriminate selling creates opportunity.

(Pictured above, select PFF Holdings over time. Note the decline since April).

In this piece I’m covering three 7%+ yielding Preferreds PFF has dumped that I believe offer attractive risk-to-reward, along with my Portfolio changes since the most recent June update. To be clear: Preferreds are almost never a “home run” investment. The higher dividend yield compensates you for lack of upside, and the regular, large dividends force taxable income every year, something you likely wouldn’t encounter with Common Stock in companies that return capital via buybacks instead. Still, if you have spare cash to deploy at a small weight (approximately 1% a position, diversification is a necessary), and want to add yield into your Portfolio, I think you may enjoy this piece.

Brief Introduction to Preferreds

Preferreds are hybrid securities that sit between Debt and Common Equity in the capital stack. If a company liquidates, Bondholders get paid first, Preferred Holders second, and Common Shareholders collect whatever is left.

Standard exchange-traded Preferreds are typically issued at a $25 Par Value, and pay a dividend quoted against that par value. For example, a $25 Par 6% Perpetual Preferred pays $1.50 annually (usually on a quarterly basis). Many Preferreds are also issued at a $50 or $100 Par Value, so it is important to read the prospectus or search for the ticker on QuantumOnline to get accurate information.

Some Preferreds are Cumulative, meaning that if a company skips a dividend, the skipped dividends accumulate and the company cannot pay anything to Common Shareholders until they pay the dividends that are in arrears to the Preferred Holders. Other Preferreds (such as Microstrategy’s STRD and most Bank Preferreds) are Non-Cumulative, meaning the company can still skip a payment, but skipped dividends vanish forever.

Nearly every Preferred is Callable at or above par value, meaning that at some point in the future, the company has the option of redeeming the Preferred and repaying cash. In practice, companies use this call option when they are able to reissue Preferreds at a lower yield. This can be when interest rates decline, or when credit quality improves. After all, why would a company keep a 7% Preferred if they can suddenly refinance at 6% or 5.5%? The Callability of Preferreds keeps this option open for them.

Of course, there are nuances way beyond what I’ve covered here. Some Preferreds are Fixed-to-Floating. The dividend is fixed for an initial period before switching to a floating rate, typically a spread over a benchmark like SOFR. Additionally, not all Preferreds from the same issuer are pari passu (Latin for equal footing), meaning that some rank higher in the Capital Stack than others, and thus carry a higher yield to compensate investors for risk (for example, Microstrategy’s STRC has liquidation preference over STRD, meaning that STRC holders must be repaid in full before STRD holders in the event of insolvency).

Still, I hope this brief introduction has brought you up to speed on the basics of Preferreds .

Now, the question is: why do people purchase them, especially given they tend to underperform Equities over time?

The answer is simple: predictable income and generally lower volatility. A 7% annual dividend may not initially sound enticing, but against a backdrop of Hynix dropping 10% more frequently than Iran and the United States agreeing to “finally end the conflict” with each other, it’s not hard to see why conservative investors prefer the steadier nature of Preferreds and the cash they provide.

Many Preferreds also carry tax advantages relative to bonds. In the United States, Preferred Stock issued by most C-Corps (most companies aside from REITs and MLPs) receives qualified dividend treatment, allowing shareholders to pay long-term capital gains rates of 0%, 15%, or 20%, instead of ordinary income rates that can be as high as 37%, on the dividend payment. In 2026, a married couple would owe zero Federal tax on qualified dividends up to $98,000, provided they have no other income. Not bad if you have a need to maximize cash income while minimizing taxes.

Preferreds express a view on a company’s credit quality. For example, if a company issues a 6% Preferred at $25 ($1.50 a year) and it drops to $15 (a 10% current yield) and you believe that 10% is inappropriately high, you can purchase the Preferred with a goal of capital appreciation in addition to yield. If the market comes around to your view and the yield re-rates 8%, the price recovers to $18.75, generating a 25% gain on top of any dividends you receive during the trade. This is really the only exception to the “no home runs” rule; when you buy a Preferred at a deep discount to par you have capital appreciation potential. Now, here are three that catch my eye.

1: Arch Capital Preferred Series G (ACGLN)

Ticker: ACGLN

Price: $16.23

Target Price: $17.00

Parent Ticker: ACGL

Parent Sector: Insurance

Dividend: $1.1375 Fixed (Paid Quarterly)

Current Dividend Yield: 7.02%

Strip Dividend Yield: 7.06%

Common Stock Market Cap: $34.43 Billion

Tangible Common Equity: $22.154 Billion

Position Weight: 1.0%

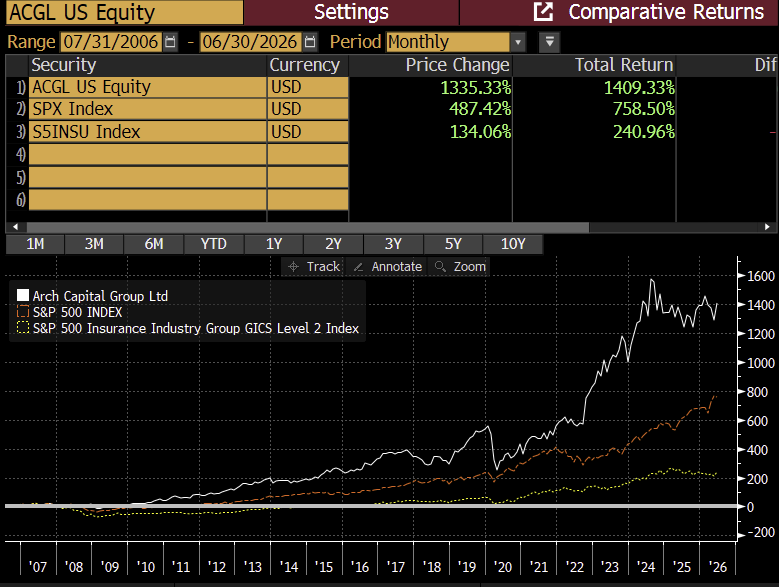

I consider Arch Capital Group to be an excellent insurer. The company is a consistent outperformer (having generated an annual return of 14% over the last 20 years as compared to 6% for the broader insurance benchmark), is well-capitalized, and conservatively run (no annual losses within the last 20 years).

The Common Stock is up roughly 5% YTD while the Preferred continues to languish - in part due to rising interest rates, but also due to nearly 400,000 shares sold by the PFF ETF over the last 12 months. Ultimately, Arch’s Preferreds sit on top of nearly $22 Billion in Tangible Common Equity (parked in Arch’s investment-grade fixed income Portfolio), well-protected and unlikely to be threatened. Arch is rated A+ by AM Best (not a credit rating, rather, an insurance rating), indicating superior performance and financial stability. Even a significant hurricane or catastrophe causing $3 - 4 Billion in losses (significantly in excess of previous events) can be readily absorbed by Arch’s balance sheet.

The Preferred has dribbled down for years, and I think constant selling from PFF has exacerbated an unusual diversion between the Preferred and Arch’s underlying Common Shares. In short, I believe 7% yield from a well-respected insurer represents a highly attractive entry point. Arch is one of the best (and largest) in the business, and a 7% yield with positive convexity if yields decline is attractive to me relative to the Common and relative to leaving my cash idle. I have allocated 1% to Arch Capital Series G here at $16.23, and am leaving another 0.5% in orders around $15.70, which would represent a 7.25% yield. Ultimately, I think Arch’s Preferreds should yield 6.50 - 6.75%, representing $16.85 - $17.50, and until then, I am happy to hold and receive 7% in qualified dividends.